Santander Foreign Income Mortgage Guide

DIRECTOR AND MORTGAGE ADVISER

Specialist broker for high-earning professionals and complex income cases.

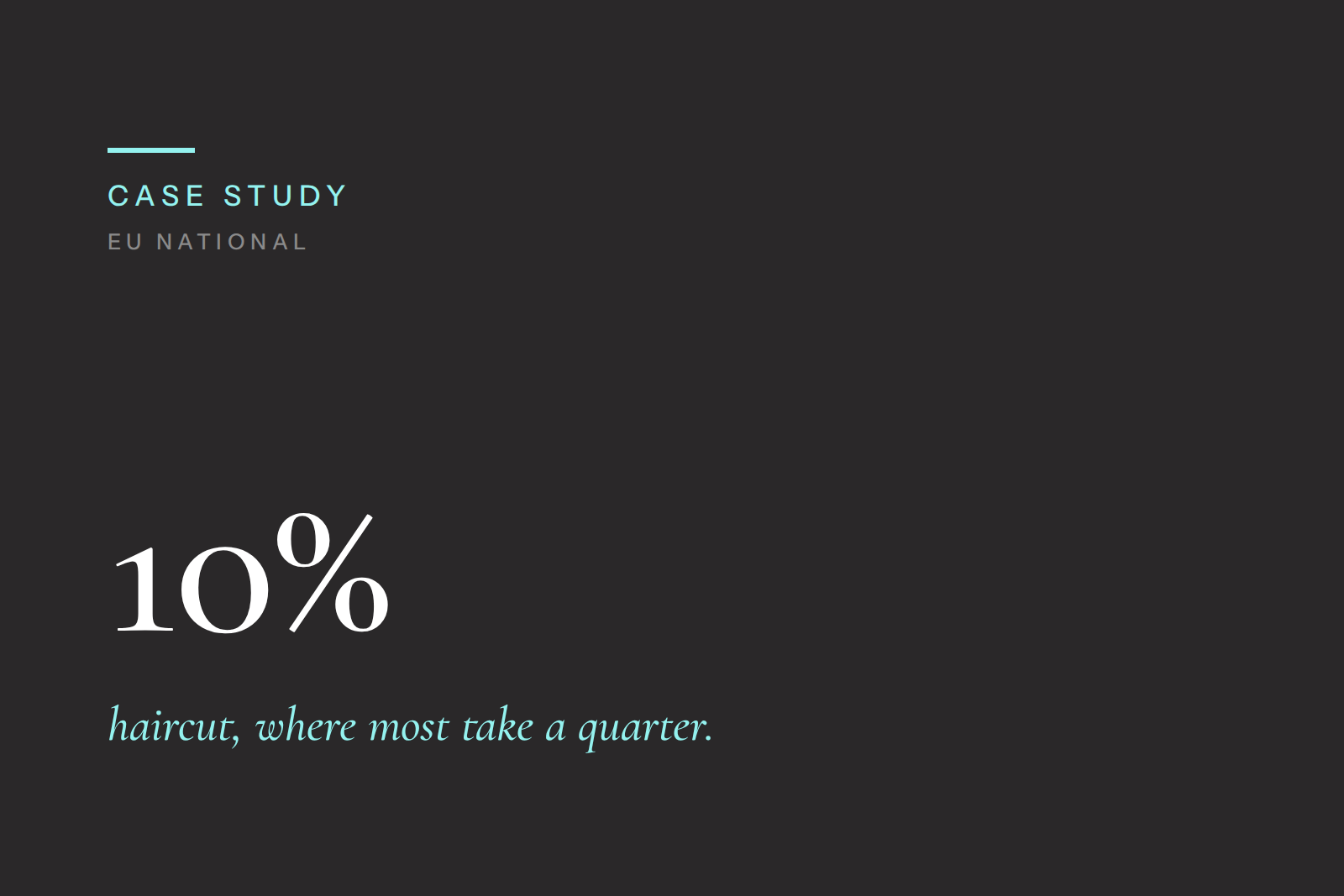

Santander is one of the few high street lenders that will accept some foreign currency income for mortgages. However, their criteria are narrower than rivals, and their 25% haircut is the steepest among the mainstream banks — meaning borrowing power is often reduced.

At Kite Mortgages, we help clients understand where Santander may work, and when another lender could provide a better fit. Our role is to structure your application correctly and compare options across the market.

Santander’s Approach to Foreign Income

Santander’s Approach to Foreign Income

Santander will consider applications where any part of employed income is paid in a foreign currency, provided it’s in one of a small list of accepted currencies.

Currencies Santander Accepts

US Dollar (USD)

Euro (EUR)

Swiss Franc (CHF)

UAE Dirham (AED)

No other currencies are accepted.

How Santander Treats Foreign Income

Non-sterling income must be converted to GBP at application stage.

25% haircut applied across all foreign income to allow for currency fluctuations.

Brokers must record:

Original foreign currency amount

GBP equivalent

Exchange rate used

Date of calculation

Income Types Accepted

Employed income only (salary, bonus, overtime, commission).

Self-employed and LLP partner foreign income not accepted.

Documentation Requirements

Payslips and bank statements showing original foreign currency income.

Proof of exchange rate used for conversion.

Request your fee free mortgage consultation today. No obligation, just sound advice.

Strengths and Limitations of Santander

Where Santander Works Well

Simple, clear criteria.

Accepts four major global currencies.

Suitable where employed foreign income is stable and straightforward.

Where Santander Falls Short

Highest haircut (25%), reducing borrowing capacity significantly.

Narrow list of accepted currencies.

Does not accept self-employed or LLP partner foreign income.

How We’ve Helped Clients Like You

These clients faced similar challenges - here’s how we helped them secure the right deal.

Alternatives to Santander

Halifax – Accepts 5 currencies (USD, EUR, AUD, INR, CHF), haircut 20%, accepts LLP partners and contractors.

HSBC – Accepts hundreds of currencies, haircut 10–30%, can also consider overseas applicants.

NatWest – Accepts 16 currencies, no haircut (uses 100% of income), but UK residency required.

Private banks – For high earners and complex cases, can often provide bespoke solutions.

Speak To An Expert Today

Get in touch for a fee free, no-obligation chat about how we might be able to help you.

Why Work with a Broker Instead of Going Direct?

With Santander’s haircut and restrictions, it’s not enough to look at rate alone. A broker ensures you see the bigger picture:

True cost of borrowing – factoring in rate, fees, charges, and penalties.

Flexibility – Santander’s products may differ in overpayment options, early repayment charges, and maximum term.

Structuring for your needs – ensuring your mortgage matches how you’re paid and your long-term plans.

Market comparison – Santander may not offer the best value if another bank will use more of your income.

Our role is to structure your mortgage in a way that protects your affordability, fits your lifestyle, and saves you time.

Next Steps

If you’re considering Santander for a foreign income mortgage, it’s important to know both the strengths and the limitations. Santander can be a good option for straightforward employed income — but in many cases, other lenders may allow you to borrow more or offer greater flexibility.

At Kite Mortgages, we’ll:

Present your foreign income correctly for Santander.

Show you how Santander compares to Halifax, HSBC, NatWest, and others.

Structure your mortgage to meet your long-term financial goals.

See our complete guide to foreign currency income mortgages →

Request your fee free mortgage consultation today. No obligation, just sound advice.

FAQs

-

USD, EUR, CHF, and AED.

-

25% across all foreign income.

-

No, only employed income.

-

Yes, but foreign income is discounted before being included.

-

It depends. For some employed applicants it works — but other lenders may allow you to borrow more.

Related Articles

YOUR HOME MAY BE REPOSESSED IF YOU DON’T KEEP UP REPAYMENTS ON YOUR MORTGAGE

Kite Mortgages is a trading style of Kite Financial Ltd which is an appointed representative of The Openwork Partnership, a trading style of Openwork Limited which is authorised and regulated by the Financial Conduct Authority.

APPROVED BY THE OPENWORK PARTNERSHIP ON 26/11/2025.