HSBC Foreign Income & Overseas Customer Mortgage Guide

DIRECTOR AND MORTGAGE ADVISER

Specialist broker for high-earning professionals and complex income cases.

If you’re a professional earning in a foreign currency — or you live and work overseas but want to buy in the UK — HSBC is one of the few high street lenders that may consider your application.

Their policies are broader than most lenders, but also more complex, with rules on acceptable currencies, haircuts, country restrictions, and minimum income levels. Navigating this successfully requires more than just filling out forms.

At Kite Mortgages, we help busy professionals and international clients present strong applications to HSBC — and compare HSBC with other lenders to ensure the best overall outcome.

Request your fee free mortgage consultation today. No obligation, just sound advice.

HSBC’s Approach to Foreign Currency Income

HSBC accepts a wide range of foreign currencies through their foreign currency matrix. This makes them one of the most flexible mainstream banks for international professionals.

Currencies HSBC Accepts

Hundreds of currencies listed in their official matrix, including USD, EUR, AUD, CAD, INR, JPY, CHF, SGD and many more.

Applicants must be from an approved country and paid in an acceptable currency.

How HSBC Treats Foreign Income

Income converted to GBP at the end of the previous month’s exchange rate.

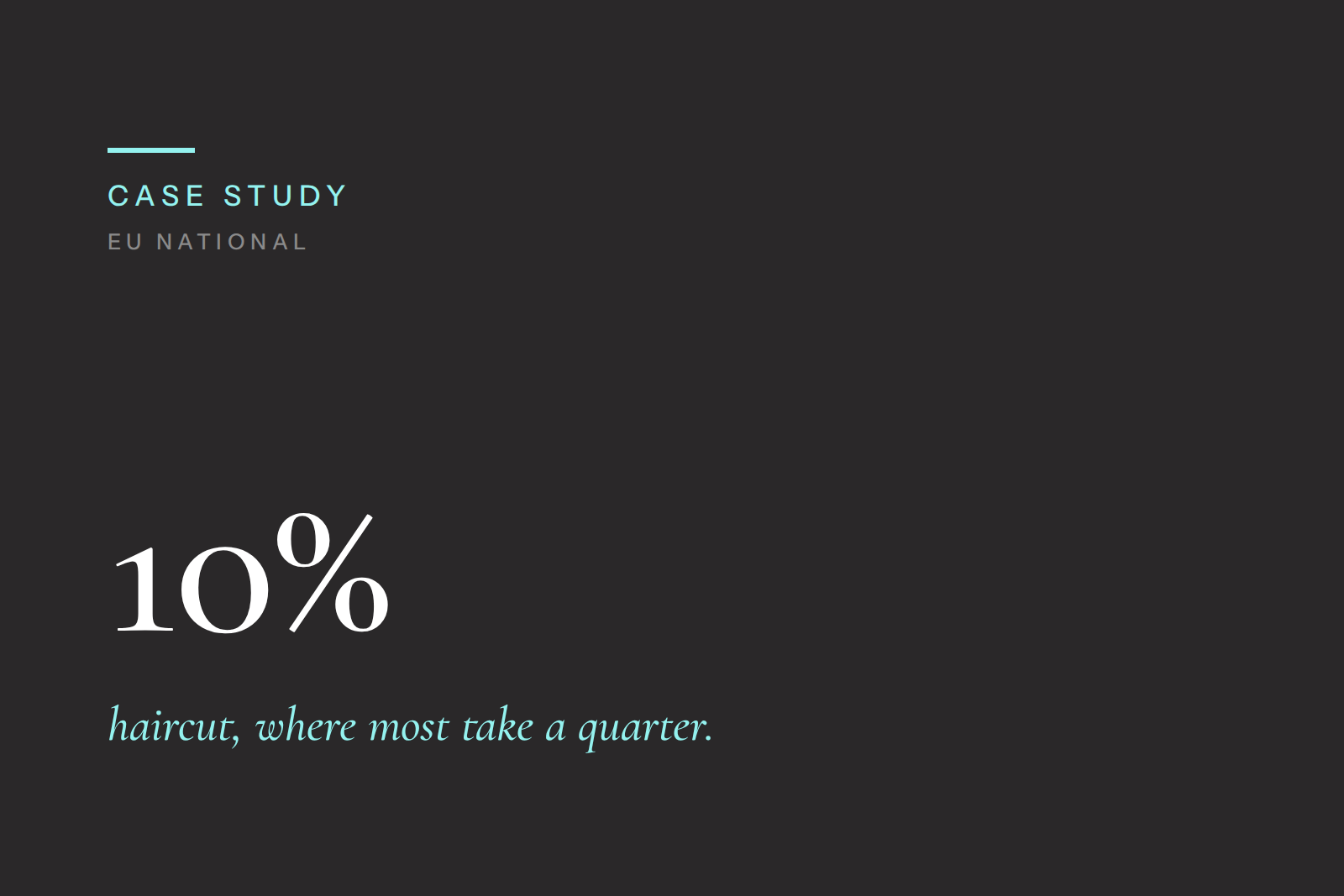

Haircut applied — typically 10%–30% depending on currency.

If FX rate drops by more than 20%, HSBC will notify customers after completion.

Documentation Required

Latest 3 months’ payslips for each income stream.

Latest 3 months’ bank statements for all non-HSBC/First Direct accounts.

Proof of residency and currency source (where required).

How We’ve Helped Clients Like You

These clients faced similar challenges - here’s how we helped them secure the right deal.

HSBC’s Overseas Customer Policy

HSBC is unusual in accepting some non-UK resident applicants. This is particularly useful for returning UK nationals, expats, and professionals based overseas.

Key Criteria for Overseas Applicants

Minimum income: £75,000 p.a. (excluding bonus/commission/overtime).

Maximum LTV: 75%.

Deposit: Must be from applicant’s own funds (not gifts/cashback).

UK bank account required to service the mortgage.

Credit report from overseas country of residence (translated if needed).

Must speak proficient English.

Country-Specific Rules

Applications are only accepted from approved countries, such as:

Australia, Hong Kong, Singapore, Switzerland, UAE, USA, and others.

Some countries (e.g. Qatar, UAE nationals) require higher income/assets or existing HSBC relationships.

Who Is Not Eligible

Applicants living in non-approved countries.

Clients permanently relocated abroad without strong UK ties.

Speak To An Expert Today

Get in touch for a fee free, no-obligation chat about how we might be able to help you.

Strengths and Limitations of HSBC

Where HSBC Works Well

One of the broadest foreign currency acceptance lists.

Can lend to non-UK residents (rare among high street lenders).

Global brand, trusted by international professionals.

Where HSBC Falls Short

Haircuts can be steep (up to 30%), reducing affordability.

Overseas applicants capped at 75% LTV.

Strict £75k minimum income threshold (excluding bonuses).

Documentation burden: payslips, bank statements, credit reports, translations.

Alternatives to HSBC

Halifax – Accepts five currencies (USD, EUR, AUD, INR, CHF), applies 20% haircut, fixed at DIP stage.

NatWest – Accepts 16 currencies, no haircut applied (100% of income used), but UK residency required.

Santander – Accepts 4 currencies (USD, EUR, CHF, AED), haircut of 25%.

Private banks – Often the best option for HNW clients or complex overseas arrangements.

See our complete guide to foreign currency income mortgages →

Why Work with a Broker Instead of Going Direct?

With HSBC, the details matter — the wrong approach can mean a declined case. A broker ensures your application is structured for success:

Currency treatment – We check haircut % and how it affects borrowing power.

True cost of borrowing – Rate is just one piece. We compare fees, charges, early repayment penalties, and offset options.

Overseas complexity – We manage international credit reports, translations, and HSBC’s country-specific rules.

Structuring the loan – Whether interest-only, long-term flexibility, or overpayment capacity, we ensure the mortgage fits your goals — not just the bank’s criteria.

Saving time and stress – For busy professionals abroad, we handle everything end-to-end.

Next Steps

If you’re considering HSBC for a foreign income or overseas mortgage, it pays to get it right first time. The rules are detailed, but with the right preparation, HSBC can be a strong option for international professionals.

At Kite Mortgages, we’ll:

Check if your currency and country are eligible.

Compare HSBC’s affordability with Halifax, NatWest, and others.

Structure your mortgage so it works for your long-term plans.

Request your fee free mortgage consultation today. No obligation, just sound advice.

FAQs

-

HSBC’s matrix includes most major world currencies. Haircuts vary from 10–30%.

-

Yes, provided you live in an approved country and meet their minimum income and LTV rules.

-

£75,000 p.a. (excluding bonus, commission, or overtime).

-

Yes, overseas applicants must hold a UK account to service the mortgage.

-

75% LTV, subject to affordability and income haircut.

Related Articles

YOUR HOME MAY BE REPOSESSED IF YOU DON’T KEEP UP REPAYMENTS ON YOUR MORTGAGE

Kite Mortgages is a trading style of Kite Financial Ltd which is an appointed representative of The Openwork Partnership, a trading style of Openwork Limited which is authorised and regulated by the Financial Conduct Authority.

APPROVED BY THE OPENWORK PARTNERSHIP ON 22/09/2025.