Do All Lenders Accept RSU Income?

DIRECTOR AND MORTGAGE ADVISER

Specialist broker for high-earning professionals and complex income cases.

If you're paid in Restricted Stock Units (RSUs), you're not alone—equity-based compensation is increasingly common, especially in tech, fintech, and private equity.

But when it comes to mortgage applications, not all lenders are on the same page. Some fully embrace RSUs, while others ignore them altogether.

Here’s what you need to know to make your RSU income work for your mortgage goals.

Request your fee free mortgage consultation today. No obligation, just sound advice.

What Are RSUs and How Do They Affect Mortgage Applications?

RSUs are a form of deferred compensation—shares awarded to you by your employer that vest over time, often on a multi-year schedule.

They can form a significant part of your total compensation package, sometimes exceeding your base salary. But for mortgage purposes, the key question is: do lenders treat RSUs as income?

The answer: some do, some don’t—and the criteria vary.

Which Lenders Accept RSUs (and Which Don’t)?

Mainstream high-street lenders often treat RSUs cautiously or ignore them altogether, focusing instead on base salary. However, select lenders—including specialist and private banks—may accept RSU income if:

It has vested consistently over the past 2–3 years

You can show regular sales of stock, or that shares are sold to generate cash

RSUs form a material, recurring part of your total compensation

Your employer is a well-known, stable company listed on a recognised exchange

Some lenders will average the actual cash proceeds from sold RSUs over the past 2–3 years, while others may only consider the vesting schedule, not actual value realised.

How We’ve Helped Clients Like You

These clients faced similar challenges - here’s how we helped them secure the right deal.

How to Strengthen Your Application with RSU Income

To make your RSU income count, prepare the following:

Vesting schedules detailing future RSU release dates and volumes

Brokerage statements showing past stock sales and proceeds received

Payslips or compensation summaries illustrating total equity value

Employer confirmation, if needed, on how RSUs are structured and awarded

The more consistent and well-documented your RSU income, the more lenders will be willing to include it as part of affordability.

Speak To An Expert Today

Get in touch for a fee free, no-obligation chat about how we might be able to help you.

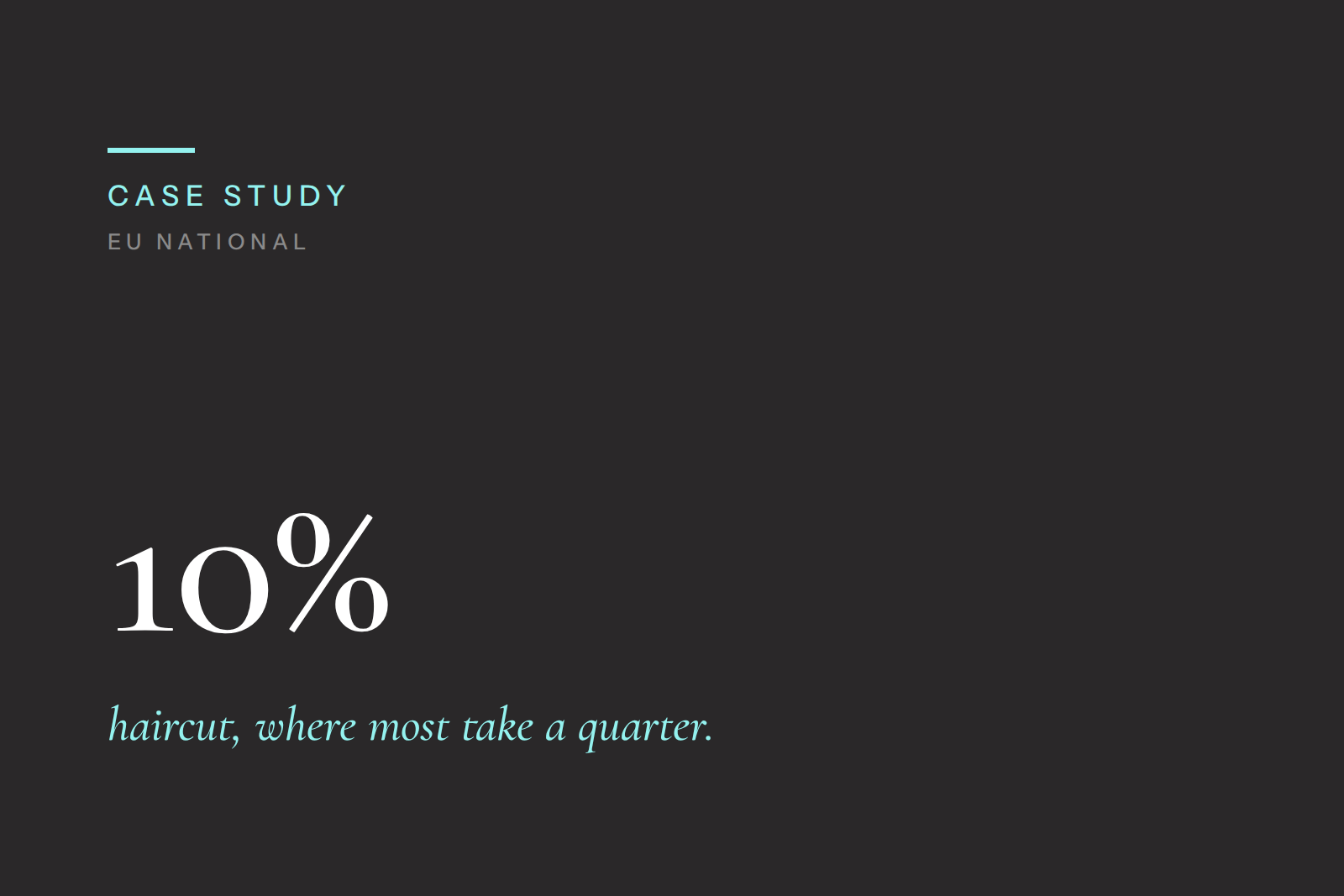

How Much of Your RSU Income Will Count?

Even among lenders who accept RSUs, treatment varies:

Some may use 100% of average RSU income over the last 2–3 years

Others may cap it at 50–75%, or apply a haircut to account for market volatility

A few may only count vested and sold RSUs—not those you’ve kept or that remain unvested

If your RSUs have only recently started vesting, some lenders may require a longer track record before they’ll factor it in.

Why Work with a Broker for RSU-Based Applications

Because RSU income is handled so inconsistently, working with a broker is critical. We help by:

Identifying which lenders will accept RSU income based on your profile

Structuring your application to highlight equity income clearly and accurately

Navigating lender-specific quirks and documentation requirements

Helping you decide whether a mainstream lender, specialist lender, or private bank is the best route

If RSUs are a core part of your earnings, a generic “salary-only” mortgage approach could undercut your true affordability.

Conclusion: RSUs Can Boost Affordability—If Used Strategically

Your equity income is valuable—but only if your lender sees it that way. With the right documentation and lender match, RSUs can meaningfully increase how much you can borrow.

Not sure where your RSUs stand with lenders?

We specialise in structuring mortgage applications for professionals with equity-based pay—ensuring your compensation is presented to its full potential.

Request your fee free mortgage consultation today. No obligation, just sound advice.

FAQs

-

Yes—if you’ve sold the shares and the proceeds are in your account, they’re treated as savings like any other asset.

-

Unvested RSUs generally won’t count as income—but some lenders may consider the future vesting schedule as part of the overall picture.

-

Unlikely. Most lenders will use an average of realised income or apply a discount to account for volatility.

-

Possibly—private lenders often offer greater flexibility with complex income structures, especially if your RSUs are substantial and ongoing.

Related Articles

YOUR HOME MAY BE REPOSESSED IF YOU DON’T KEEP UP REPAYMENTS ON YOUR MORTGAGE

Kite Mortgages is a trading style of Kite Financial Ltd which is an appointed representative of The Openwork Partnership, a trading style of Openwork Limited which is authorised and regulated by the Financial Conduct Authority.

APPROVED BY THE OPENWORK PARTNERSHIP ON 19/09/2025.