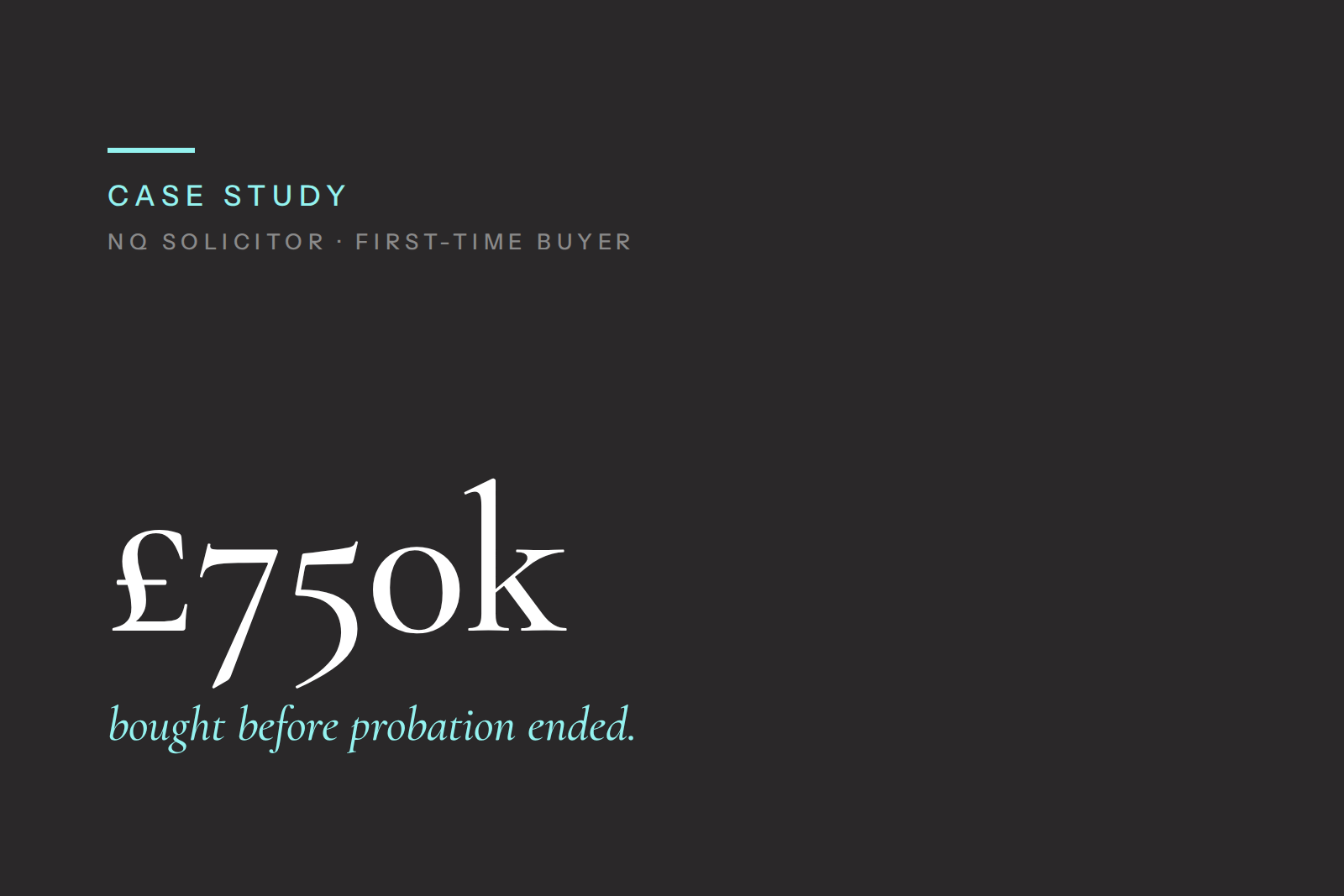

Professional Mortgages For Solicitors: Newly Qualified First Time Buyer

DIRECTOR AND MORTGAGE ADVISER

Specialist broker for high-earning professionals and complex income cases.

Request your fee free mortgage consultation today. No obligation, just sound advice.

Overview

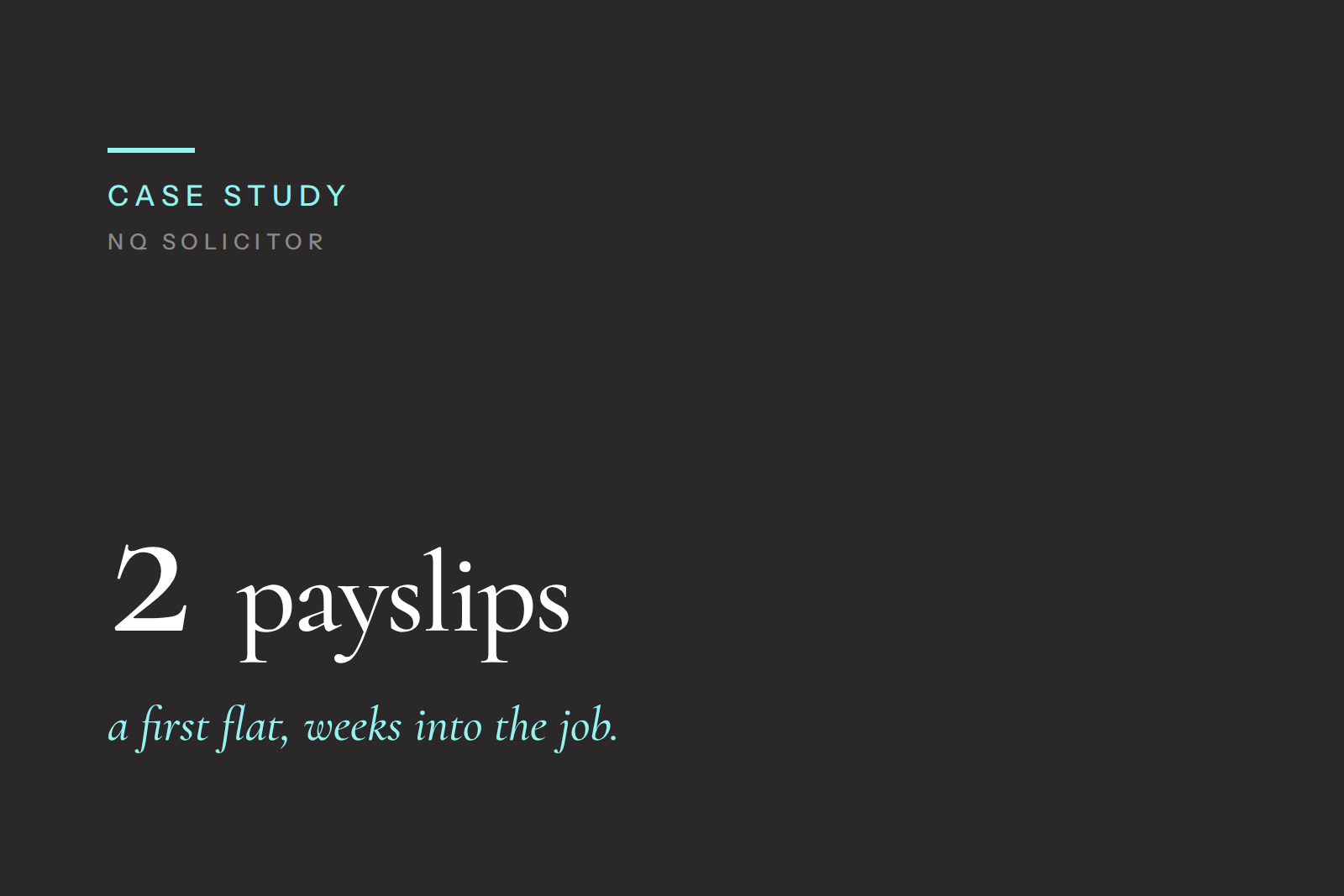

A newly qualified (NQ) solicitor had just moved from trainee to associate and wanted to buy her first home. With only an offer letter and initial payslips to hand—and still within a probation period—she needed a lender prepared to consider early‑career professional cases. Our job was to present a clear, sustainable picture of income and affordability.

Client Snapshot

Profession: Solicitor (NQ), private practice

Status: Recently qualified; limited time in role; probation in force

Income: Base salary confirmed in offer letter; discretionary bonus TBD

Goal: First‑time buyer mortgage with manageable payments

Concerns: Whether limited payslip history and probation would block approval

The Challenge

Short Track Record: Only one to two payslips; new employer and role.

Probation & Policy: Many lenders prefer 3–6 months in role; probation can restrict options.

Evidence Of Progression: Need to explain the step‑up from trainee pay to NQ salary.

Affordability Clarity: Student loan, pension, and professional subscriptions affect net income.

Speak To An Expert Today

Whatever it is, the way you tell your story online can make all the difference.

What We Did

Matched The Case To Professional Criteria: Shortlisted lenders that may consider NQ lawyers using offer letters, contracts and first payslips.

Told The Income Story: Explained the move from trainee to NQ, mapped salary uplift to the contract, and excluded any unproven bonus from affordability.

Provided A Clean Evidence Pack: Contract/offer letter, first payslips, bank statements, proof of deposit/source of funds, HR email confirming start date and probation terms.

Modelled Conservatively: Used base salary only, after typical deductions (student loan, pension), and ensured buffers for bills and rate changes.

Kept It Simple For Underwriting: Short covering note linking each number to a document to avoid back‑and‑forth.

The Outcome

Approval With A Mainstream Lender that accepts early‑career professionals (subject to evidence).

Manageable Payments based on base salary; scope to review terms at future remortgage once the track record builds.

Smooth Process: Offer issued within the seller’s timeline; completion coordinated with solicitor and agent.

Why It Worked

Right Lender Fit: Professional criteria suitable for early‑career lawyers.

Clear, Conservative Packaging: Base‑salary‑only affordability with transparent deductions.

Documentation First: Offer letter + payslips + HR confirmation answered the key questions upfront.

Documents We Provided (Typical For NQ Solicitors)

Employment contract/offer letter confirming base salary and start date

First payslips and bank statements showing salary credit

HR confirmation of probation terms (where available)

Proof of deposit and source of funds

ID & address verification

Thinking Of Doing Similar?

We help newly qualified solicitors and early‑career lawyers present a clear, conservative case so the right lender can make a straightforward decision.

Request your fee free mortgage consultation today. No obligation, just sound advice.

Quick FAQs

-

Some lenders may consider applications during probation, especially for professionals, where documentation is clear.

-

In some cases, yes. Some lenders may work from a signed contract/offer plus first payslip(s) and bank evidence of credit.

-

Usually the current contract salary. Bonuses are often excluded until a track record is shown.

-

Varies. Many lenders prefer 3–6 months in role, but some may accept less for professionals with strong evidence.

-

Often. Most lenders will consider gifts from close family with the right paperwork.

Related Case Studies

YOUR HOME MAY BE REPOSESSED IF YOU DON’T KEEP UP REPAYMENTS ON YOUR MORTGAGE

Kite Mortgages is a trading style of Kite Financial Ltd which is an appointed representative of The Openwork Partnership, a trading style of Openwork Limited which is authorised and regulated by the Financial Conduct Authority.

APPROVED BY THE OPENWORK PARTNERSHIP ON 24/09/2025